Pinching Pennies

Understanding the landscape of debt in America

Last Updated

The average household in America owes more than $96,000 in debt.

The average household in America owes more than $96,000 in debt.

These bills add up quickly between credit cards, student loans, and car payments. Considering the 2021 median household income in the U.S. was around $71,000, household debt is uncomfortably high compared to total household earnings.

To understand the landscape of debt in America, we polled 2,000 people and asked them how and when they learned about finance, and how often they live paycheck to paycheck. Continue reading to see the financial state of our nation.

Financial Adulthood

There comes a time when you finally realize paying with a credit card isn't the same as paying with cash. Deciding when to pay outright for something versus financing—or financing over time—is a big part of financial adulthood.

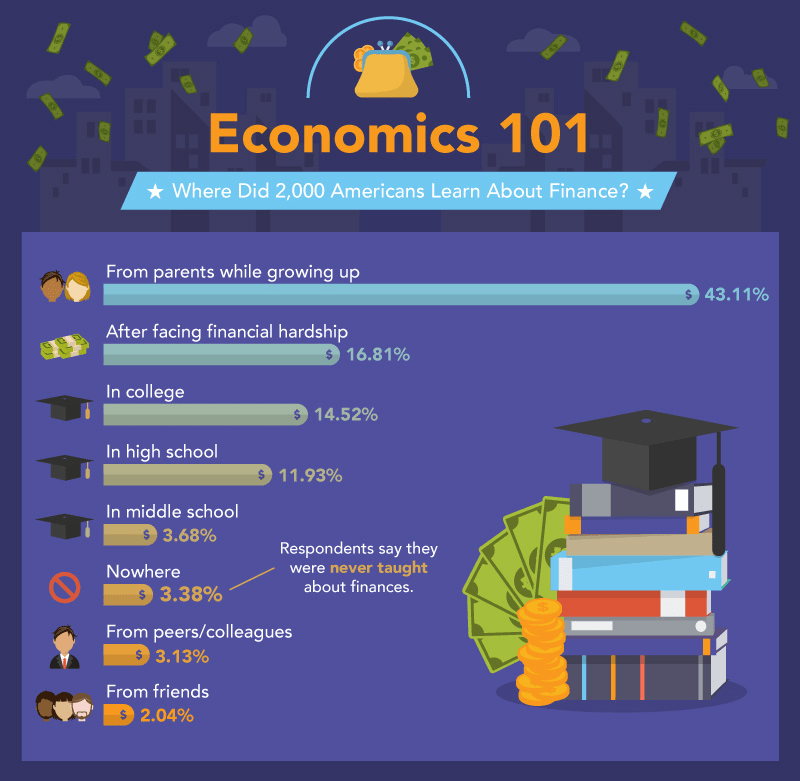

We asked our survey respondents where they learned about finance. Overwhelmingly, over 43 percent said they learned from their parents while growing up. Parents are an integral part of how well we understand finance and debt.

For nearly 17 percent of respondents, that lesson only came after enduring financial hardship. Maybe they struggled for the first time making a car payment or got behind on a credit card. Unfortunately, having to worry about money is a lesson all on its own.

For others, their financial lesson came from school. Almost 15 percent said they learned finance in college, while around 12 percent learned about it in high school, and about 4 percent picked it up in middle school.

Learning and Living in Debt

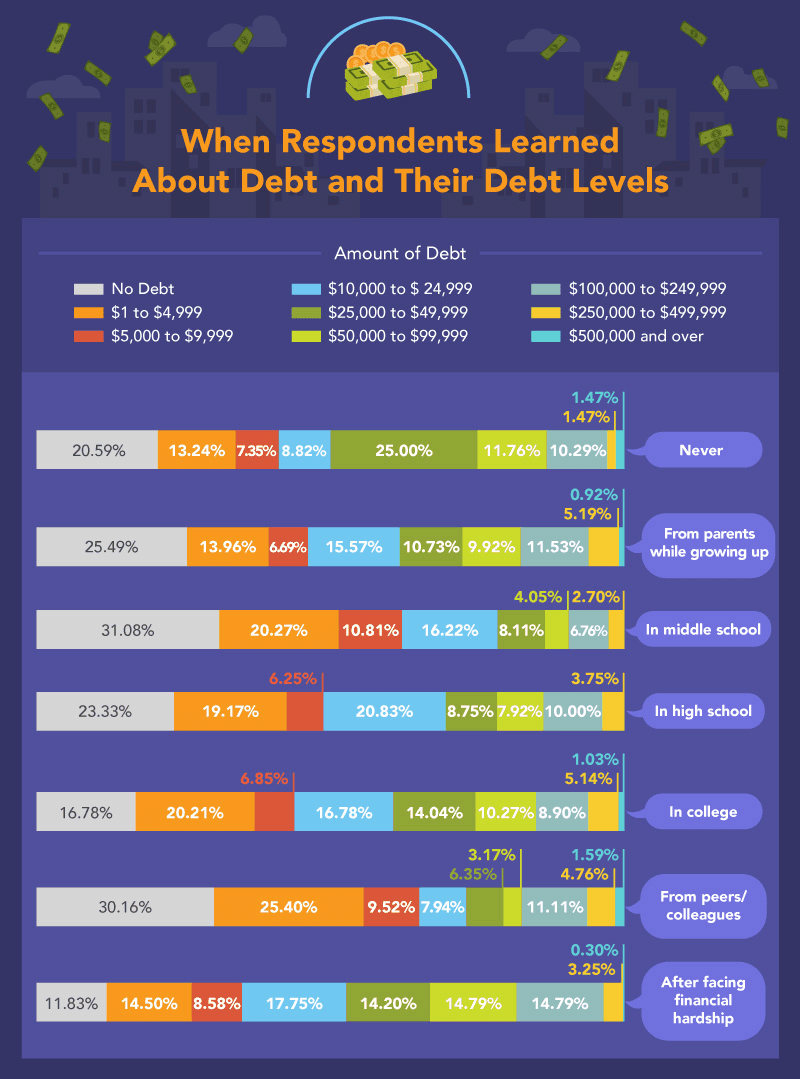

Those who learned about the rigors and repercussions of debt in middle school were the most likely to report no debt at the time of our survey. Over 31 percent had no debt, and around 20 percent owed less than $5,000. We leave our childhood behind and enter our teenage years in middle school—those who learned about finance before high school were better for it.

Survey respondents who picked up their debt lessons from peers and colleagues were also more likely to report lower debt levels, with just over 30 percent owing nothing at all.

Unfortunately, for some, the lessons came too late. Those who learned about debt after facing personal financial hardship were the most likely to report having between $100,000 and $249,000 in debt. Not learning the ins and outs of financial responsibility in time can eventually cause significant repercussions when figuring out how to pay that money back.

Financial Lessons

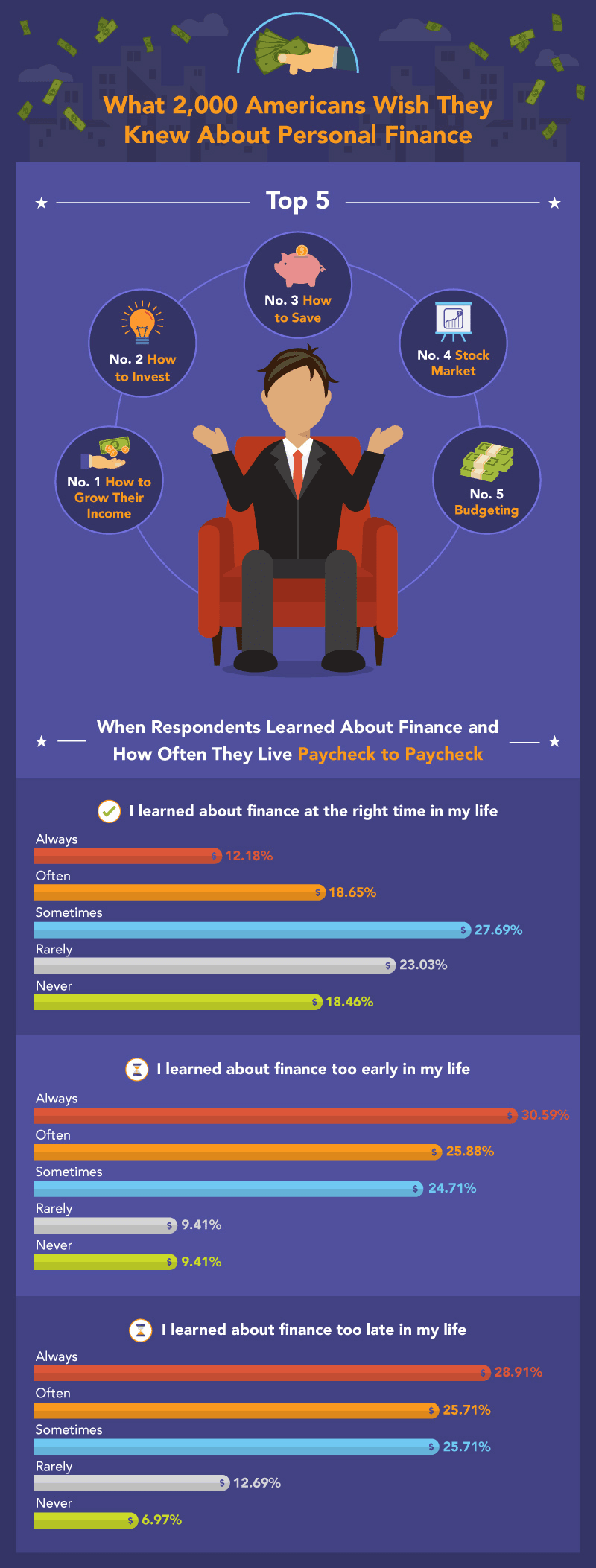

Financial education can have its growing pains. Sometimes, lessons about saving money and making a budget can come too late. Most survey participants wished they knew more about growing their income.

Only about 53 percent of Americans have enough money in savings to cover a $500 emergency, while many people live paycheck to paycheck. Understanding saving and investing could help alleviate unnecessary stress. The burden of living paycheck to paycheck can mean having enough money to cover bills and immediate needs, but not enough to put additional money aside for long-term investments, like retirement or buying a home. By better understanding personal finance rules like budgeting and growing your income, you may be able to avoid the harsher lessons brought on by debt.

For those who are always living paycheck to paycheck, over 30 percent said they felt they learned about finance too early in life. For those who sometimes, rarely, or never live paycheck to paycheck, their financial education came at exactly the right time.

A sound understanding of good financial habits helps create financial stability that can last for years to come.

Money Matters

Whether from student loans or credit cards, debt is no laughing matter. Depending on how well you understand finance, you may find yourself in certain financial debt without fully realizing how it happened.

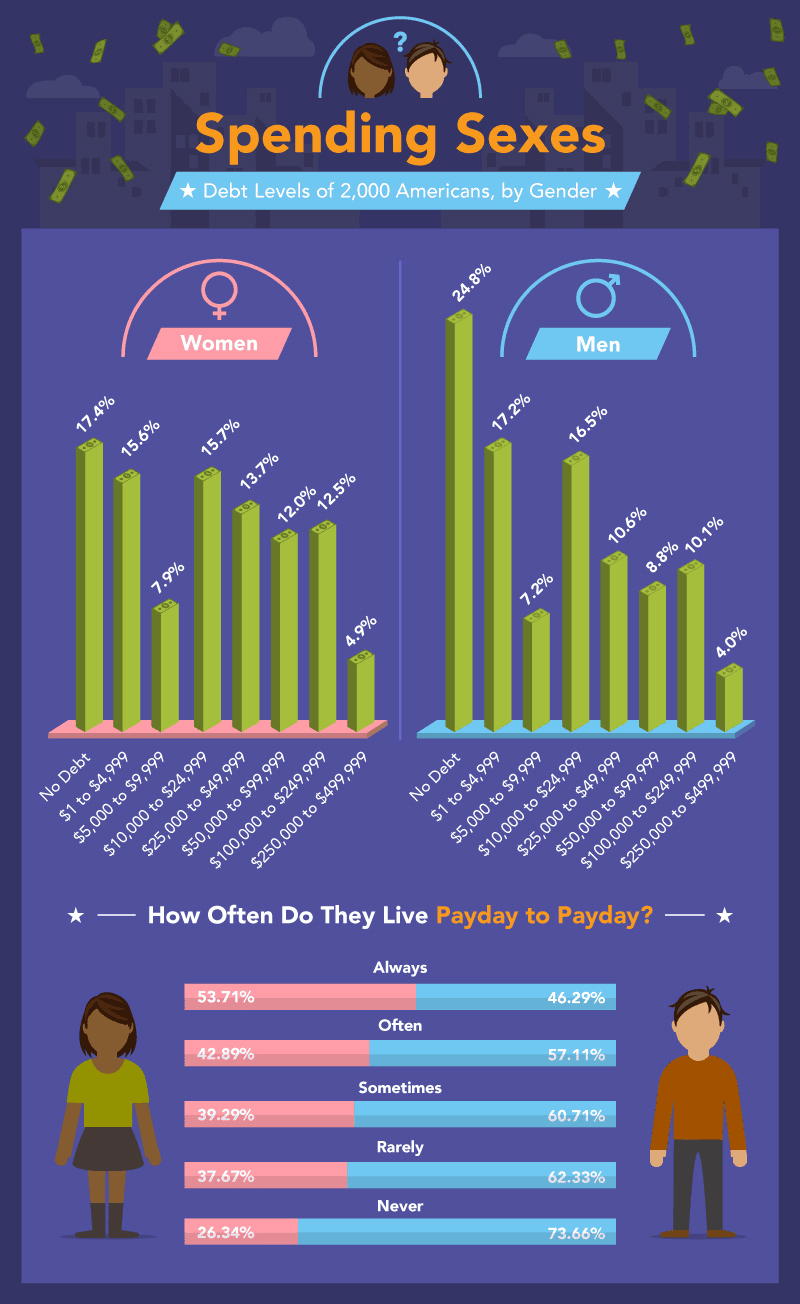

According to our survey, women were more likely to find themselves in debt. While just over 17 percent of women reported no debt, almost 25 percent of men were able to say the same. Thankfully, less than 16 percent of female respondents and a little over 17 percent of male respondents reported having accrued less than $5,000 in debt. Depending on how much you earn, the amount of debt you take on might take years to pay off. Less than five percent of women reported between $250,000 and $499,999 in owed money.

Women were also more likely to report always having to live paycheck to paycheck (nearly 54 percent), while men were more likely to report never living paycheck to paycheck (almost 74 percent).

Lessons Learned

Regardless of when you learn about financial security or where those lessons come from, the most important thing is that you understand how money really works. From debt and interest rates to the stock market and investing, your financial education can be the difference between earning enough to live comfortably (and saving a little on the side) and being forced to live paycheck to paycheck to cover life's expenses.

At Trade-schools.net, you can explore budget-friendly opportunities to continue your education and find the programs that will teach you about some aspects of finance you may feel you missed out on.

While most Americans have some form of debt, you can still take steps today to secure your financial future. Learning how to budget appropriately, save in addition to paying bills and costs, and investing savings can create financial stability that pays you back in money and peace of mind. You can't put a price on that.

Methodology

We surveyed 2,000 people in the U.S. to find out how they learned about personal finance, how prepared they were for their current financial situation, and their current debt levels to explore how financial education may lead to less debt and financial struggles.

Additional Source

- Forbes, 63% Of Americans Don't Have Enough Savings To Cover A $500 Emergency, website last visited on June 23, 2020.

Want to Share This?

Financial education is essential, so please share our content with your readers for non-commercial purposes only. Just give our authors proper credit.